As I look in the rearview mirror, 2021 was our best year yet in real estate. Despite being masked for most of the year, the pandemic raged but our clients continued to buy and sell homes. Now in November, 2022, America and many other countries are experiencing the highest inflation in forty years – as a result of skyrocketing energy costs and pandemic related supply chain disruptions. What does this mean for the housing market? In the last three years, since the pandemic started, the US has seen the steepest, most dramatic home price increase in history. What’s next? I dug in, drilled down, and found some interesting and troublesome trends for the near future of housing prices.

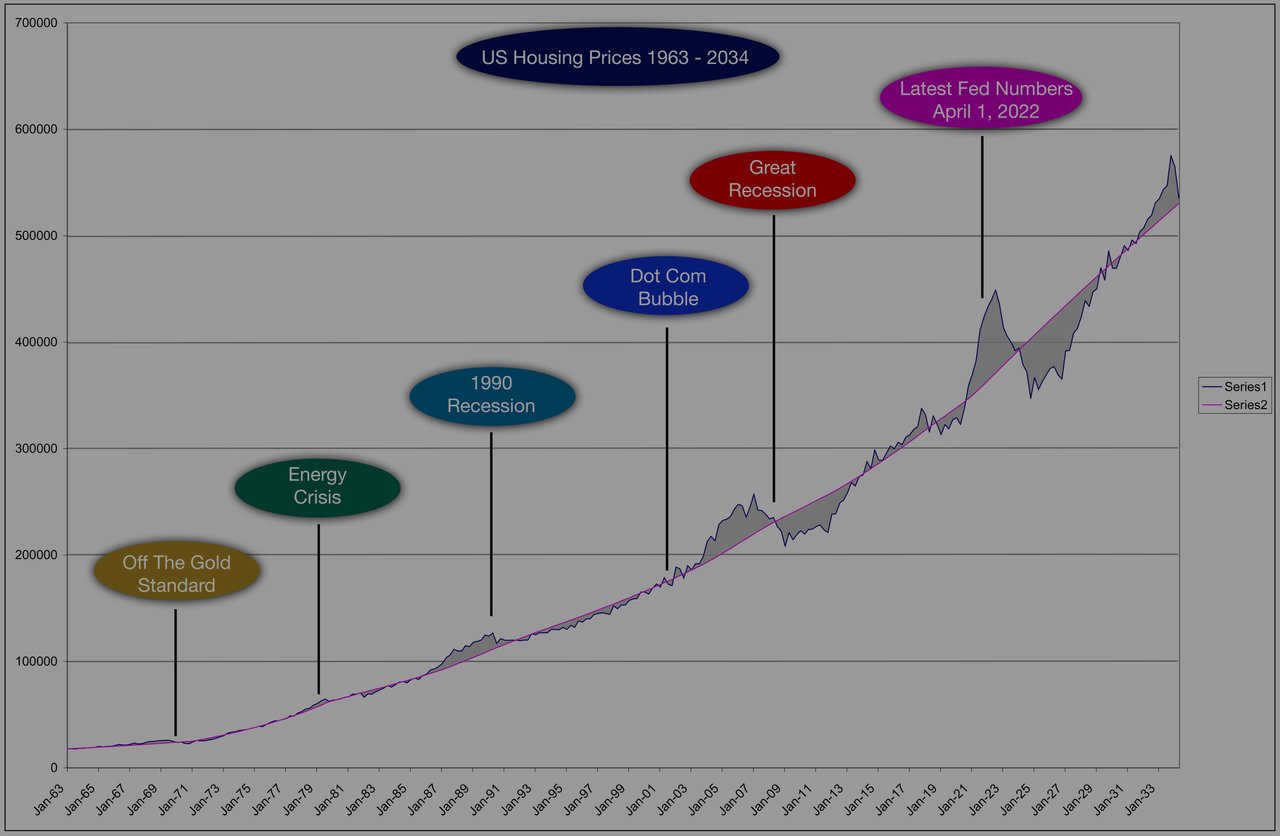

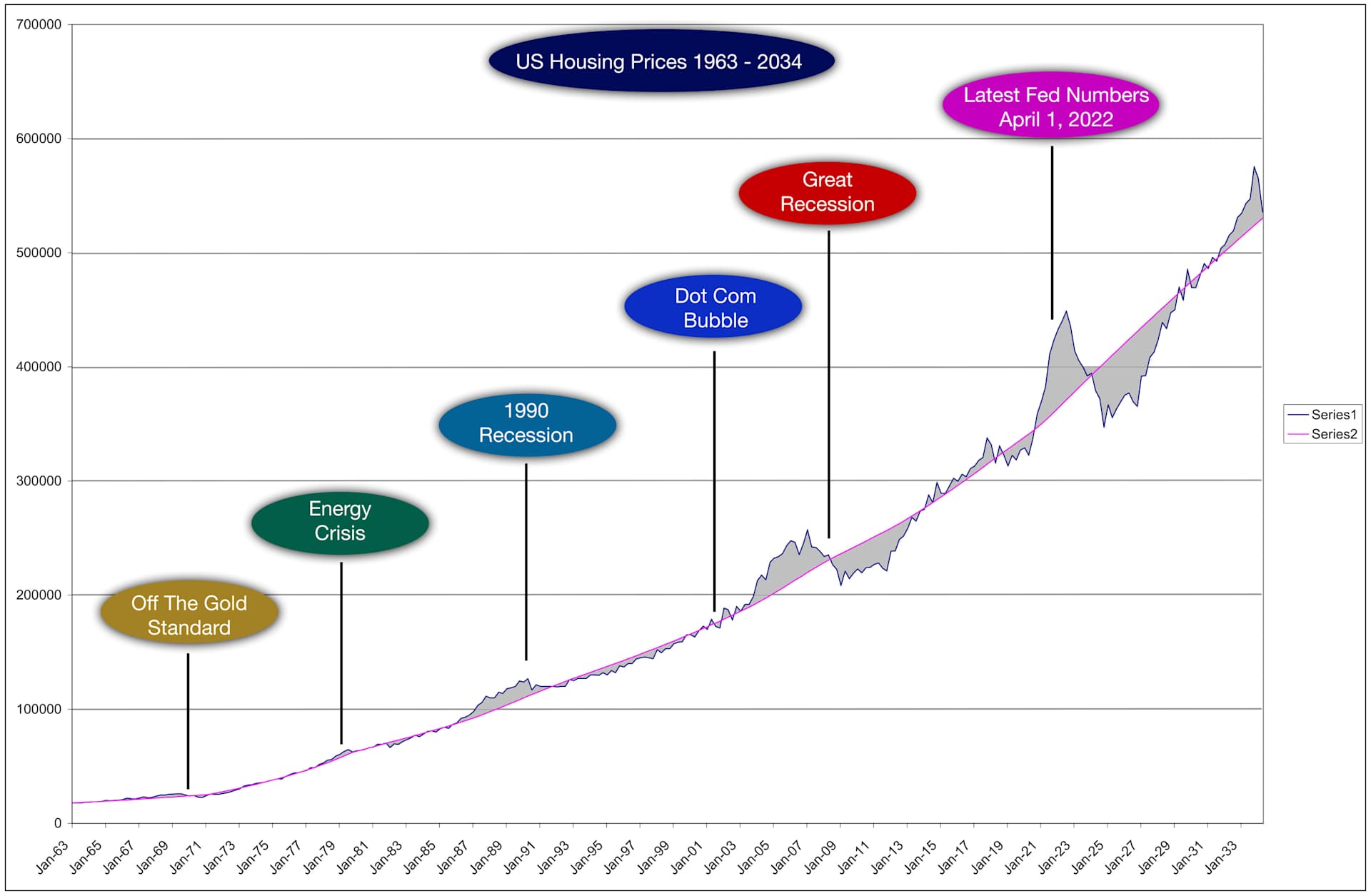

The St. Louis Federal Reserve Bank provides collections of relevant housing data from HUD (Housing an Urban Development) and the Census Bureau. I dropped in the pink trend line. The blue line is SLFRB’s median home price. These are the ups and downs of that indicator. Price changes are never a straight line. Some quarters saw prices increase, others had declines. Each data point is a quarter going back to 1963 (extending those points into the future I'll go into later). There are several prolonged periods in which the prices were consistently above the trend line or below it. I looked at five specific prolonged peaks and valleys: 1. Early 1970's - When the US left the Gold Standard, 2. The 1979 - 1980 Energy Crisis, 3. The 1990 Recession, 4. The 2001 Dot Com Bubble, and 5. The 2008 Great Recession.

I noticed several cyclical trends.

In each of these five events there was a peak above the trend line and then a valley after it. In every case, the valley lasted at least as long as the peak which preceded it. In the case of the 1990 Recession; the valley was the longest, 50% longer than the peak, 11 quarters above the trend and 19 quarters below.

As the median home value has increased over the years, the deviation above and below the trend line continues to grow greater in dollars. In the 1970’s the largest ripple was $1,400. The decline in the Great Recession from the peak to the valley was $50,000. And now, based on that decline we could be seeing median decrease of $100,000 next year, just fifteen years on from the Great Recession.

Not all cycles are created equal. While the Dot Com Bubble caused an economic recession, the recovery in home prices occurred within 12 months. In context, the median home price change looks like a blip on the graph, but it was terrible time for the economy.

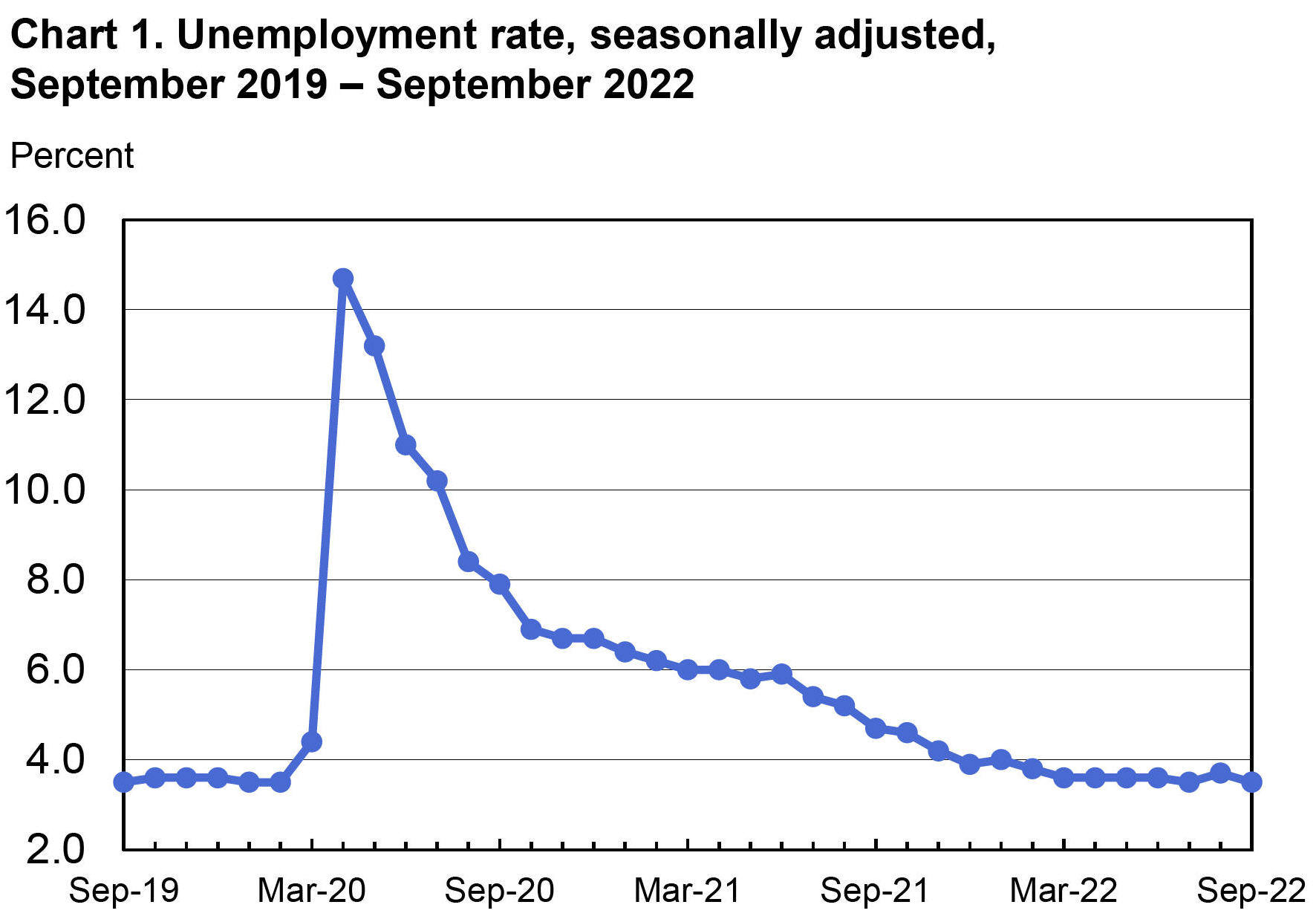

After the Great Recession, some new controls (and stress tests) were put in place to make banks and Wall Street less vulnerable to the mortgage backed securities, the sub-prime market, and derivatives debacle which resulted in the housing bubble and then bust. What is happening now – we hear – is a “different” type of national financial crisis. We’ve not had a recession with all time low unemployment (3.5%). It’s not the type of recession we’ve seen before.

So what’s in store ahead? No one is making wild guesses. We are hearing experts cautioning that a recession is around the corner -- if it hasn’t already started (one of the key indicators, two quarters of negative GDP growth we’ve just experienced in Q1 and Q2, October saw a slight increase in GDP). When it comes to home prices, we can certainly see trends from the historical record.

In my graph figure, I extend out the trend line from the latest available Fed data (thru April 1, 2022) and replicated the data swing percentages based on the Great Recession historical record. The data reveals a variance of $100,000, from nearly $450,000 to $350,000 in the next year. That value would be recovered near the end of 2028, six years from now. I write that the value will be recovered because based on history, home values have always recovered.

The modeling will be affected, of course, by every economic input. The Federal Reserve will attempt a “soft landing” (which the Federal Reserve always attempts but has never achieved). Their only tool is a sledge hammer, adjusting the prime lending rate, and they’ve been using it. Interest rates have been going up dramatically for months and sales activity has all but stopped for those who will be financing their home purchase.

Policy and law makers will extol the virtues of their many bills to come, to curb any pains of a recession on their constituents because, of course, the lead up to the 2024 general election will overlap this recession.

Geo-political affairs will directly impact -- by extending or shortening how these numbers unfold -- the length of the next recession and the next recovery. Among these are; Russia and the war in Ukraine, tensions with China and its Taiwan issues, and those problems on the Korean peninsula. Too, how the worldwide energy crisis and skyrocketing inflation will affect the recovery and depth of the recession.

As important is business and consumer confidence. Will business begin to curtail investment and will unemployment rise as it has in past recessions? We do not see unemployment increasing yet, and there are still 10.1 million unfilled jobs.

In our consumer driven economy, will consumer confidence slip along with our spending habits and cause even further economic contraction?

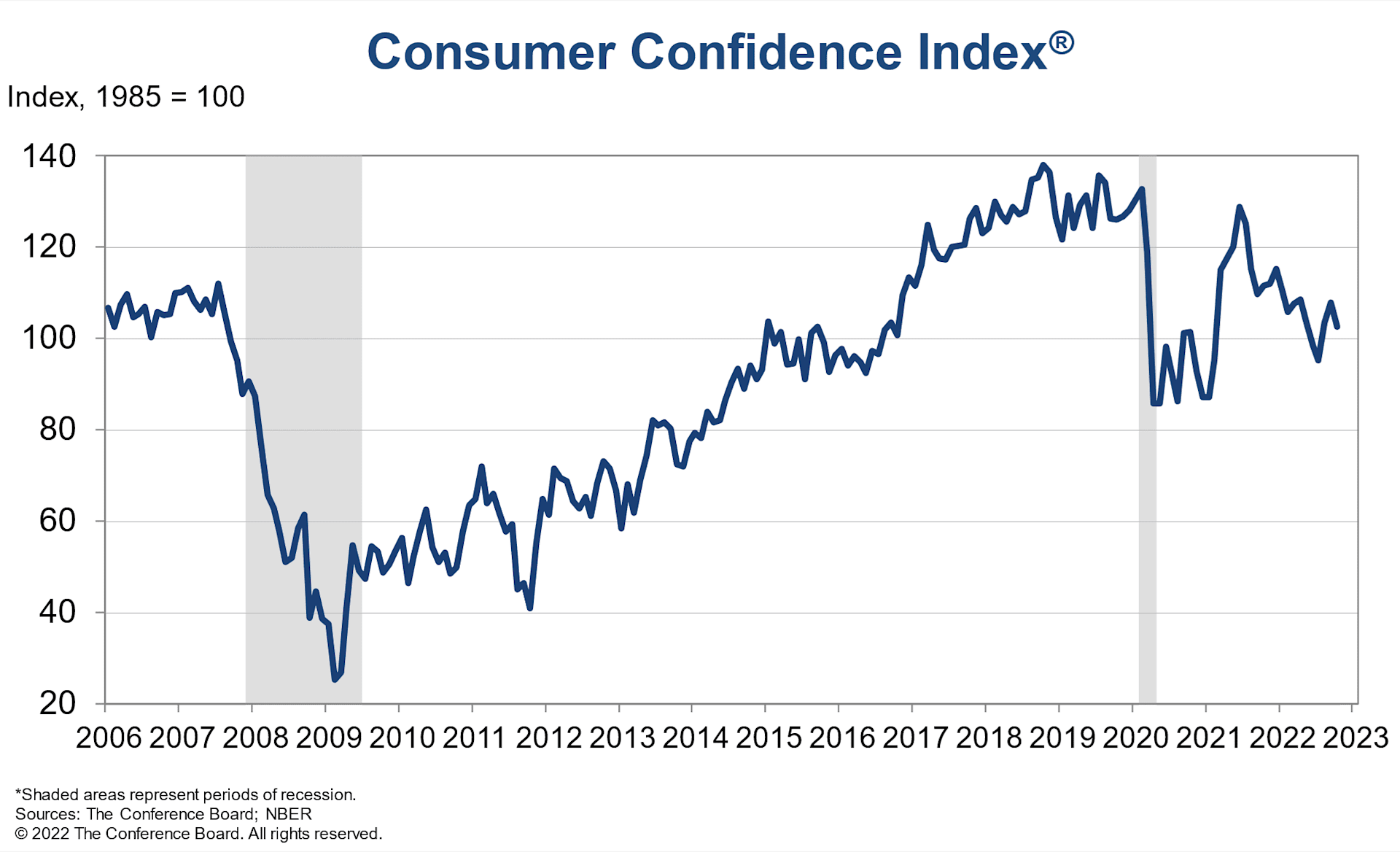

“Consumer confidence retreated in October, after advancing in August and September,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “The Present Situation Index fell sharply, suggesting economic growth slowed to start Q4. Consumers’ expectations regarding the short-term outlook remained dismal. The Expectations Index is still lingering below a reading of 80—a level associated with recession—suggesting recession risks appear to be rising.”

While we have mixed indicators, the 2022 CEO Outlook from KPMG says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . . More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

As Ali Wolf, Chief Economist at Zonda, explains: “Housing is traditionally one of the first sectors to slow as the economy shifts but is also one of the first to rebound.”

Since this may be a “different” kind of recession, we can hope that history doesn’t repeat itself. Perhaps cooler heads will prevail abroad and the guard rails installed a decade ago will maintain us on our economic road better than we experienced in the past. If that's the case, looking behind us is just a cautionary peek in the rearview mirror “Objects may be closer than they appear.”